CA Inter Audit Notes – Chapter 6: Audit Documentation (SA 230)

Exam-Oriented Notes | ICAI | Quick Revision + Important Points

Chapter Overview

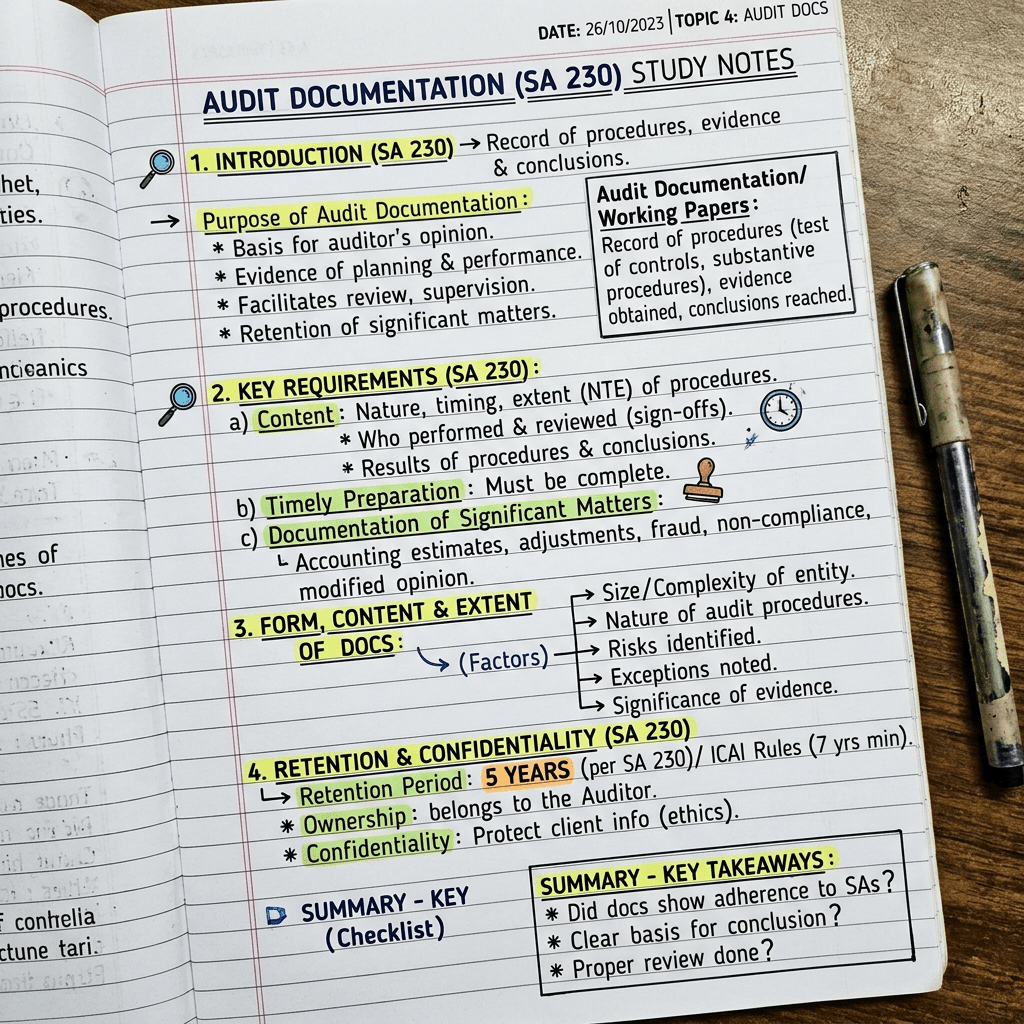

SA 230 – Audit Documentation

Audit Documentation means the written record of:

- Audit procedures performed

- Audit evidence obtained

- Conclusions reached by the auditor

Also known as:

- Working Papers

- Work Papers

1. Definition of Audit Documentation

Audit Documentation refers to the record of:

- Audit procedures performed

- Relevant audit evidence obtained

- Conclusions reached by the auditor

Remember:

Documentation = Procedures + Evidence + Conclusions

2. Objectives of Audit Documentation (Very Important)

The auditor should prepare documentation that provides:

(a) Basis for Auditor’s Report

A sufficient and appropriate record supporting the auditor’s opinion.

(b) Evidence of Compliance

Evidence that audit was:

- Properly planned

- Properly performed

- Conducted according to Standards on Auditing (SAs)

- Conducted according to legal requirements

Easy Mnemonic

BE

- B → Basis of Audit Report

- E → Evidence of compliance with SAs

3. Nature of Audit Documentation

Audit documentation provides evidence that:

- Auditor achieved overall audit objectives.

- Audit complied with SAs.

- Audit complied with legal and regulatory requirements.

4. Purposes of Audit Documentation (Very Important)

Audit documentation helps in:

1. Planning the audit

2. Supervising and reviewing audit work

3. Making engagement team accountable

4. Maintaining records for future audits

5. Quality Control Reviews (SQC 1)

6. External inspections by regulators

Mnemonic

PSAQER

- P – Planning

- S – Supervision

- A – Accountability

- Q – Quality Control

- E – External Inspection

- R – Record for Future Audits

5. Form, Content and Extent of Audit Documentation

Documentation should enable an experienced auditor (with no previous connection) to understand:

(a) Nature, timing and extent of audit procedures

(b) Results of audit procedures and audit evidence

(c) Significant matters

(d) Conclusions reached

(e) Professional judgments made

Auditor should record:

Identification of items tested

Person who performed audit work

Date of completion

Reviewer

Date and extent of review

Auditor should also document:

- Discussions with management

- Discussions with Those Charged with Governance (TCWG)

- Significant matters discussed

- Date of discussion

- Person with whom discussion took place

If inconsistent evidence exists

Auditor should document:

- Nature of inconsistency

- How inconsistency was resolved

6. Factors Affecting Form, Content & Extent

Depends upon:

- Size and complexity of entity

- Nature of audit procedures

- Risk of material misstatement

- Significance of audit evidence

- Nature and extent of exceptions

- Need for documenting conclusions

- Audit methodology and tools

Mnemonic

SNR SENT

- S Size

- N Nature

- R Risk

- S Significance of evidence

- E Exceptions

- N Need for conclusion

- T Tools & methodology

7. Examples of Audit Documentation

Includes:

- Audit programmes

- Analyses

- Issue memoranda

- Summary of significant matters

- Confirmation letters

- Representation letters

- Checklists

- Correspondence (including emails)

May also include:

- Contracts

- Agreements

NOT Included

Do not include:

- Superseded drafts

- Preliminary notes

- Corrected copies

- Duplicate documents

8. Timely Preparation

Documentation should be prepared:

On a timely basis

Advantages:

- Better quality

- Easier review

- Accurate documentation

- Strong audit evidence

Late preparation is less reliable.

9. Audit File

Meaning

Audit file means:

One or more folders (physical/electronic) containing audit documentation for one engagement.

10. Assembly of Final Audit File (Very Important)

The auditor should assemble audit documentation:

After the date of the auditor’s report.

Time Limit

Within 60 days

after the date of auditor’s report.

Administrative Changes Allowed

- Removing old documents

- Cross referencing

- Sorting papers

- Signing checklists

- Documenting evidence already obtained

NOT Allowed

No:

- New audit procedures

- New conclusions

11. Retention Period (Exam Favourite)

Audit documentation should be retained for:

Minimum 7 years

from:

- Auditor’s report date

OR - Group auditor’s report date (whichever is later)

12. Documentation of Significant Matters

Examples include:

- Significant risks

- Material misstatements

- Change in risk assessment

- Difficult audit procedures

- Modified opinion

- Emphasis of Matter

Professional Judgment should also be documented

Examples:

- Basis of important conclusions

- Reasonableness of estimates

- Authenticity of documents

13. Completion Memorandum (Audit Documentation Summary)

Contains:

- Significant matters identified

- How those matters were resolved

Benefits:

- Easy review

- Easy inspection

- Helpful in large audits

- Helps ensure compliance with all SAs

14. Ownership of Audit Documentation (Very Important)

Audit documentation belongs to:

Auditor

NOT the client.

Auditor may provide extracts to client if:

- It does not affect audit quality.

- Independence is not impaired.

Important Time Limits

| Particular | Time |

|---|---|

| Assemble Final Audit File | Within 60 days |

| Retention Period | Minimum 7 years |

Important Exam Points

✔ SA Applicable → SA 230

✔ Working Papers = Audit Documentation

✔ Property of → Auditor

✔ Audit File → Physical/Electronic records

✔ Timely preparation improves audit quality

✔ No new audit procedures after report date

✔ Final audit file within 60 days

✔ Retention period = 7 years

Mnemonics for Revision

Objectives

BE

- B → Basis of Report

- E → Evidence of Compliance

Purpose

PSAQER

- Planning

- Supervision

- Accountability

- Quality Control

- External Inspection

- Record for Future Audits

Factors Affecting Documentation

SNR SENT

- Size

- Nature

- Risk

- Significance

- Exceptions

- Need for conclusion

- Tools

ICAI Exam Questions Frequently Asked

- Define Audit Documentation.

- Objectives of Audit Documentation.

- Purposes of Audit Documentation.

- Factors affecting form, content and extent.

- Examples of Audit Documentation.

- Explain Audit File.

- Assembly of Final Audit File.

- Time limit for assembly (60 days).

- Retention period (7 years).

- Ownership of Audit Documentation.

- Completion Memorandum.

- Documentation of Significant Matters.

One-Page Revision Sheet

- SA: 230

- Meaning: Procedures + Evidence + Conclusions

- Objectives: Basis of report + Evidence of compliance

- Purposes: Planning, Supervision, Accountability, Future audits, QC, Inspection

- Documentation Includes: Audit programme, Analyses, Checklists, Confirmation, Representation letters, Emails

- Audit File: Physical/Electronic folders of audit documentation

- Final File Assembly: Within 60 days

- Retention: 7 years

- Ownership: Auditor

- No new audit procedures after audit report

- Completion Memorandum: Significant matters + Resolution

Leave a comment