Lesson 1: Nature, Objective and Scope of Audit – Exam Notes

1. Meaning of Audit

Definition:

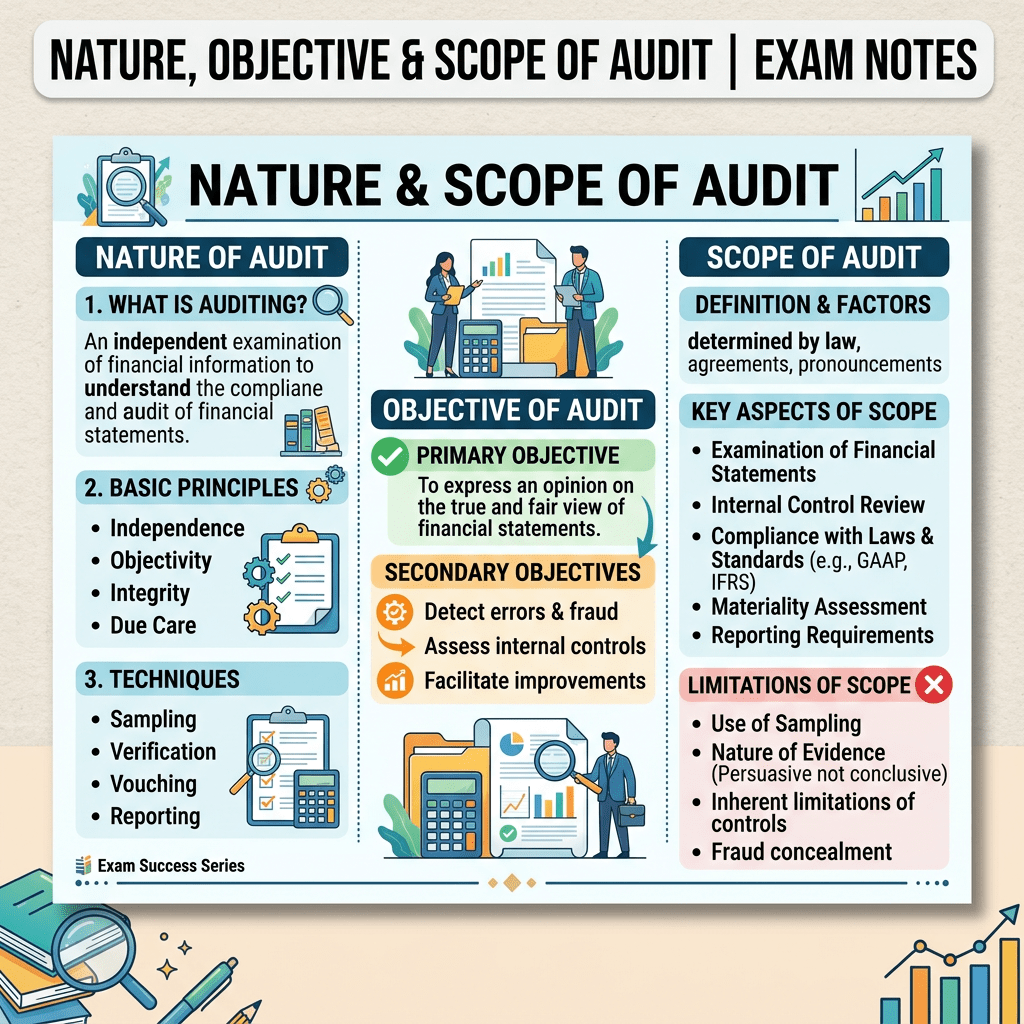

“An audit is an independent examination of financial information of any entity, whether profit-oriented or not, irrespective of size or legal form, conducted with a view to expressing an opinion thereon.”

Key Features

- Independent Examination

- Auditor must be free from influence.

- Independence ensures objectivity.

- Examination of Financial Information

- Includes financial statements and accounting records.

- Applicable to Any Entity

- Company, LLP, Partnership, Trust, NGO, Society, etc.

- Purpose: Expression of Opinion

- Auditor gives opinion through audit report.

2. Nature of Audit

Audit Provides Assurance

- Audit increases confidence of users in financial statements.

- It provides reasonable assurance, not absolute assurance.

Responsibilities

| Management | Auditor |

|---|---|

| Preparation of Financial Statements | Expression of Opinion |

| Maintenance of Books | Verification & Reporting |

3. Origin of Auditing

Historical Background

- References found in Kautilya’s Arthashastra (4th Century BC).

- Word Audit derived from Latin word “Audire” meaning “To Hear”.

- ICAI established in 1949 for regulating Chartered Accountancy profession in India.

4. Interdisciplinary Nature of Auditing

Auditing is linked with several subjects:

(a) Accounting

- Audit reviews accounting records and financial statements.

(b) Law

- Knowledge of Companies Act, Tax Laws, etc.

(c) Economics

- Understanding economic environment.

(d) Behavioural Science

- Interaction with management and employees.

(e) Statistics & Mathematics

- Sampling techniques.

(f) Data Processing

- EDP/Computerized Auditing.

(g) Financial Management

- Ratio Analysis

- Working Capital

- Funds Flow

(h) Production

- Understanding business operations.

5. Objectives of Audit (SA 200)

Primary Objectives

1. Obtain Reasonable Assurance

Financial statements are free from material misstatements caused by:

- Fraud

- Error

2. Express an Opinion

Whether financial statements are prepared in accordance with the applicable financial reporting framework.

3. Report Findings

Issue audit report and communicate findings.

Reasonable Assurance vs Absolute Assurance

| Reasonable Assurance | Absolute Assurance |

|---|---|

| High level assurance | Complete guarantee |

| Audit provides this | Audit cannot provide this |

Exam Point: Audit provides High but not 100% assurance.

6. Scope of Audit

What Audit Includes

1. Coverage of All Relevant Aspects

Audit should be planned to cover all significant areas.

2. Reliability and Sufficiency of Information

Auditor evaluates:

- Books of account

- Vouchers

- Bills

- Documents

3. Proper Disclosure

Ensures:

- Proper classification

- Adequate disclosure

- Compliance with Accounting Standards and Law

4. Expression of Opinion

Final outcome is audit report.

What Audit Does NOT Include

Auditor is NOT:

❌ Engineer

❌ Valuation expert for technical assets

❌ Expert in authentication of documents

❌ Investigator

Audit vs Investigation

| Audit | Investigation |

|---|---|

| General purpose | Specific purpose |

| Broad scope | Narrow scope |

| Reasonable assurance | Detailed examination |

7. Inherent Limitations of Audit

Because of these limitations, audit cannot provide absolute assurance.

(1) Nature of Financial Reporting

- Management judgments involved.

- Internal controls may fail.

(2) Nature of Audit Procedures

- Sample checking.

- Auditor cannot verify every transaction.

- Possibility of fake documents.

- Management may conceal fraud.

(3) Audit is not Investigation

- No search powers.

- No power to record statements on oath.

(4) Timeliness Constraint

- Information loses relevance over time.

(5) Future Events

- Future uncertainties cannot be predicted.

Mnemonic:

FNITF

- F – Financial Reporting

- N – Nature of Procedures

- I – Investigation (Not)

- T – Timeliness

- F – Future Events

8. Engagement

Meaning

An arrangement under which auditor agrees to provide services to a client.

Engagement Letter

Formal agreement between auditor and client.

9. Benefits of Audit

Advantages

- High-quality financial information.

- Safeguards shareholders’ interests.

- Moral check on employees.

- Helps tax authorities.

- Assists lenders and banks.

- Detects frauds and errors.

- Identifies control weaknesses.

10. Audit – Mandatory or Voluntary?

Mandatory Audit

Examples:

- Companies Act Audit

- Tax Audit

Voluntary Audit

Done because of benefits and stakeholder confidence.

11. Appointment of Auditor

Generally Appointed By:

- Owners

- Shareholders

- Partners

- Government authorities (where applicable)

Company Auditor

Appointed by shareholders in AGM.

Government Company Auditor

Appointed by the Comptroller and Auditor General of India (CAG).

12. Audit Report

Submitted To

The person who appoints the auditor.

Examples:

- Company → Shareholders

- Firm → Partners

13. Assurance Engagement

Meaning

An engagement where a practitioner provides a conclusion to increase users’ confidence in information.

Elements of Assurance Engagement

5 Elements

- Three-party relationship

- Appropriate subject matter

- Suitable criteria

- Sufficient appropriate evidence

- Written assurance report

Mnemonic:

TPSEW

- T = Three Party Relationship

- P = Proper Subject Matter

- S = Suitable Criteria

- E = Evidence

- W = Written Report

14. Audit vs Review

| Basis | Audit | Review |

|---|---|---|

| Assurance | Reasonable | Limited |

| Level | High | Moderate |

| Procedures | Extensive | Fewer |

| Example | Statutory Audit | Interim Review |

15. Types of Assurance Engagements

(A) Reasonable Assurance Engagement

Example:

- Audit of Financial Statements

(B) Limited Assurance Engagement

Example:

- Review of Financial Statements

(C) Other Assurance Engagements

Examples:

- Prospective Financial Information

- Internal Control Reports

16. Qualities of an Auditor

Important Qualities

- Integrity

- Independence

- Tact

- Patience

- Judgement

- Reliability

- Professional Competence

- Knowledge of Accounting

- Clear-headedness

17. Engagement Standards

Types

1. Standards on Auditing (SA)

Audit of historical financial information.

Examples:

- SA 200

- SA 230

- SA 315

- SA 500

- SA 700

2. Standards on Review Engagements (SRE)

Examples:

- SRE 2400

- SRE 2410

3. Standards on Assurance Engagements (SAE)

Examples:

- SAE 3400

- SAE 3420

4. Standards on Related Services (SRS)

Examples:

- SRS 4400

- SRS 4410

18. Standards on Quality Control (SQC)

SQC 1

Purpose:

- Ensure compliance with professional standards.

- Ensure quality control within firms.

- Ensure appropriate reports are issued.

19. Why Standards Are Needed?

- Global benchmarks.

- Improve reporting quality.

- Promote uniformity.

- Enhance professional skills.

- Ensure audit quality.

Exam Quick Revision

Definition of Audit

Independent examination of financial information to express an opinion.

Audit Provides

✅ Reasonable Assurance

Audit Does NOT Provide

❌ Absolute Assurance

Objectives of Audit

- Reasonable assurance

- Express opinion

- Report findings

Inherent Limitations

FNITF

- Financial reporting

- Nature of procedures

- Investigation (not)

- Timeliness

- Future events

Elements of Assurance Engagement

TPSEW

- Three-party relationship

- Proper subject matter

- Suitable criteria

- Evidence

- Written report

Engagement Standards

SA + SRE + SAE + SRS

Quality Control Standard

SQC 1

Most Important SA for Chapter 1

SA 200 – Overall Objectives of the Independent Auditor and Conduct of Audit

Leave a comment